I still remember the sinking feeling in my gut when I was 22.

I had just backed my beat-up sedan into a concrete pillar in a parking garage. The bumper was hanging off like a loose tooth. I wasn’t worried, though. I thought, “Hey, I’m a responsible adult. I pay for car insurance every month. They’ll fix this, right?”

I called my agent, feeling proud of myself. Then came the cold splash of reality.

“Well,” the agent said, “The repairs are estimated at $600. Your deductible is $1,000.”

Silence.

“So… you guys pay nothing?” I asked.

“Exactly. In fact, filing this claim might actually raise your rates, even though we aren’t paying out a dime.”

I hung up, feeling cheated and confused. I paid premiums faithfully, yet when I needed help, my wallet took the hit.

If you are reading this, you’re probably staring at a policy document or a quote screen, asking the same question I did: What is a deductible in insurance? And more importantly, how do I stop it from ruining my budget?

I’ve spent the last decade navigating the insurance industry, helping friends and clients untangle these messy terms. Grab a coffee. I’m going to walk you through this so you never get blindsided as I did.

The “Cover Charge” of Insurance

Let’s strip away the corporate speak.

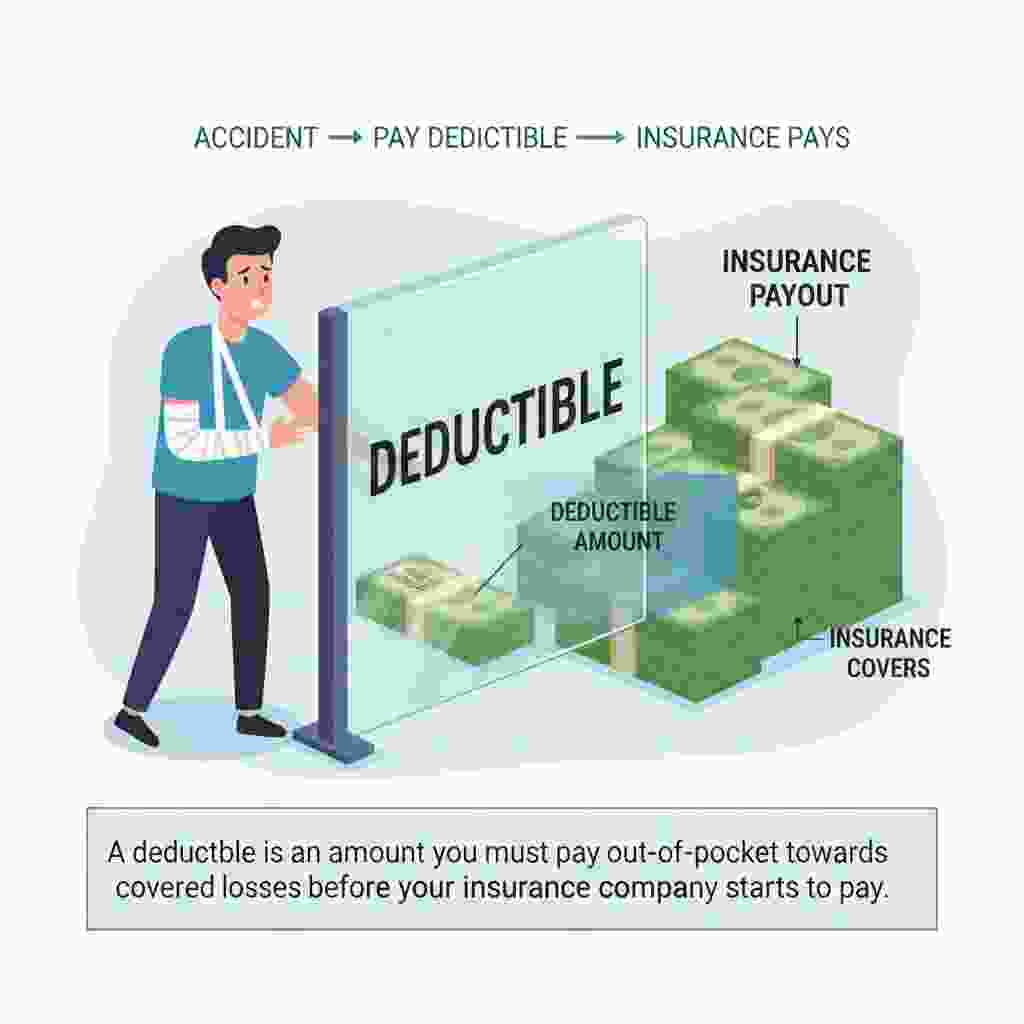

Think of an insurance deductible as the cover charge to get into the club of “The Insurance Company Paying for Your Stuff.”

It is the specific amount of money you must pay out of your own pocket before your insurance provider chips in a single cent to cover a claim.

If your policy says you have a $500 deductible, and you have a $5,000 accident:

- You pay the first $500.

- The insurance company pays the remaining $4,500.

If the damage is only $400? You pay all of it. The insurance company stays home.

Why Do Deductibles Even Exist?

You might wonder why you have to pay anything at all if you’re already paying monthly premiums. It comes down to two things:

- Risk Sharing: It keeps you careful. If repairs were 100% free, people might drive recklessly or neglect their homes. Having “skin in the game” makes us more responsible.

- Stopping Small Claims: Insurance companies don’t want to handle the paperwork for a $50 scratch on your car door. It costs them more in admin fees than the scratch is worth—the deductible acts as a barrier to filter out the small stuff.

The High vs. Low Deductible Dilemma

This is the number one question I get asked at dinner parties once people find out what I do.

“Should I choose a high deductible or a low deductible?”

There is no “right” answer, but there is a mathematical answer. It works like a see-saw.

- Low Deductible ($250 – $500): You pay more every month in premiums (the bill you pay to keep the policy active).

- High Deductible ($1,000 – $2,500+): You pay less every month in premiums.

The “Sleep Well at Night” Test

Here is how to decide without guessing.

Choose a Low Deductible if:

- You have a strict monthly budget, but you don’t have much in savings.

- If a $1,000 emergency hit you tomorrow, you’d have to put it on a credit card.

- You drive in high-risk areas or have kids who play sports (high likelihood of accidents).

Choose a High Deductible if:

- You have a solid emergency fund (at least 3-6 months of expenses).

- You are financially disciplined.

- You prefer to bet on yourself. You are willing to take the risk that you won’t crash in exchange for keeping more cash in your pocket every month.

How Deductibles Work Across Different Policies

Not all deductibles behave the same way. This is where people get tripped up. The way your car insurance treats a deductible is totally different from how your health plan does it.

1. Auto Insurance: The “Per Incident” Rule

In car insurance, the deductible usually applies per claim.

If you hit a fence in January, you pay your deductible. If you back into a mailbox in March, you pay that deductible again. It doesn’t matter that you already paid it once that year.

- Expert Note: You usually have two different deductibles on a car policy: Collision (hitting things) and Comprehensive (theft, fire, hail). You can set these at different amounts. I recommend keeping your Comprehensive deductible lower because those claims are rarely your fault.

2. Homeowners Insurance: The “Percentage” Trap

This is the sneakiest trick in the book.

Standard deductibles are flat fees (like $1,000). But many modern policies, especially in areas prone to hurricanes or windstorms, use a Percentage Deductible.

This isn’t a percentage of the damage; it’s a percentage of your home’s insured value.

- Scenario: Your house is insured for $400,000.

- Your policy has a “2% Wind/Hail Deductible.”

- A storm rips off your roof. Damage is $15,000.

- Your deductible is 2% of $400,000 = $8,000.

- The insurance pays: $7,000. You pay: $8,000.

Check your policy declaration page today. If you see a percentage sign next to your deductible, make sure you have that cash in the bank.

3. Health Insurance: The “Annual Accumulator”

Health insurance is the nice guy here (rare, I know). Your deductible is usually annual.

Once you pay enough medical bills to hit your deductible amount for the year (say, $2,000), you are done paying the deductible for the rest of the calendar year. After that, you usually just pay a smaller share (copays or coinsurance) until you hit your Out-of-Pocket Maximum.

- Watch Out For: Family deductibles. Sometimes the whole family has to hit a collective number (like $4,000) before benefits kick in for anyone. Other plans have “embedded” deductibles where once one person hits their limit, they are covered, even if the family hasn’t hit the big number yet.

The “Secret Sauce”: The Break-Even Analysis

Most people guess when picking a deductible. Don’t guess. Do the math. Here is the pro-move I use with my clients to save them hundreds of dollars a year. It’s called the Break-Even Analysis.

Let’s say you are looking at car insurance quotes:

- Option A: $500 Deductible. Premium cost: $1,200/year.

- Option B: $1,000 Deductible. Premium cost: $1,000/year.

The Math:

By choosing Option B (higher risk), you save $200 a year in premiums.

The difference in risk is $500 ($1,000 deductible – $500 deductible).

Calculation: $500 (risk difference) ÷ $200 (annual savings) = 2.5 years.

The Result:

If you can go 2.5 years without filing a claim, the higher deductible pays for itself. Everything after that is pure profit in your pocket.

If you are a safe driver, take the bet. If you are prone to accidents, stick to the lower deductible.

The “Hidden” Costs No One Tells You About

While we are discussing what a deductible in insurance is, we have to talk about the things that don’t look like deductibles but act like them.

Waiting Periods (The Time Deductible)

In Disability Insurance or even some Pet Insurance policies, you might not have a dollar-amount deductible. Instead, you have a “waiting period” or “elimination period.”

If you get sick and can’t work, the policy might say, “We pay after 30 days.” That first month of lost income? That’s your deductible. You pay it with your time and lost wages.

The “Vanishing” Deductible

Some insurers offer a “Diminishing Deductible” or “Vanishing Deductible” as a loyalty perk. For every year you go without a claim, they knock $50 or $100 off your deductible.

- My Advice: This is a great marketing gimmick, but check the math. Often, the policies with this feature cost more upfront. Are you paying an extra $50 a year to potentially save $50 later? Usually, it’s not worth it unless it’s included for free.

Your Step-by-Step Action Plan

Okay, we’ve covered the theory. Now I want you to take action. Insurance is boring, so do this quickly and get back to your life.

Step 1: The Wallet Check

Look at your savings account right now. What is the absolute maximum amount of money you could write a check for today without panicking?

- $500?

- $1,000?

- $5,000?

Write that number down. This is your deductible ceiling. Never choose a deductible higher than this number, no matter how cheap the monthly premium is.

Step 2: The Policy Audit

Dig up your declarations page (the first page of your policy packet).

- Auto: Check if your Collision deductible is higher than $500. If you have an older car (10+ years), ask yourself if you even need Collision coverage. If the car is worth $3,000 and your deductible is $1,000, you are paying premiums to protect very little value.

- Home: Look for that sneaky percentage sign (%) next to “Wind/Hail.” If it’s there, calculate the dollar amount immediately so you know your exposure.

Step 3: The “Self-Funded” Strategy

This is the ultimate financial hack.

- Raise your deductible to the highest level you can afford (based on Step 1).

- Take the money you save on monthly premiums (let’s say it’s $40/month).

- Set up an automatic transfer of that $40 into a high-yield savings account.

In three years, you will have nearly $1,500 saved plus interest. You have now self-insured your deductible. If you crash, the money is there. If you don’t crash, you keep the money—not the insurance company.

Keep that money in your pocket. You’ve earned it

I learned my lesson that day in the parking garage. I was paying for a policy I didn’t understand, assuming “full coverage” meant “free repairs.”

Now you know better.

A deductible isn’t a punishment; it’s a tool. It allows you to control your monthly costs. The key is to find the sweet spot where the monthly savings are high enough to justify the risk, but the deductible is low enough that it won’t bankrupt you on a bad Tuesday.

Here is your CTA (Call to Action):

Don’t wait for a disaster to find out what your deductible is. Log in to your insurance portal today. If your savings have grown since you first bought the policy, raise your deductible. Stop paying the insurance company forrisksk you can handle yourself.